Bookkeeping

Straight Line Basis Calculation Explained, With Example

When you use the straight-line depreciation formula, the expense journal entry will be the same each year. The primary benefit of accelerated depreciation is an increased cash flow in the early years of owning an asset, allowing businesses to reinvest these funds into their operations or other assets. Additionally, faster write-offs can lead to reduced taxable income and a lower tax liability each year.

How Does Accelerated Depreciation Work?

Straight-line depreciation posts the same amount of expenses each accounting period (month or year). But depreciation using DDB and the units-of-production method may change each year. OpEx, which covers items like salaries and overheads, refers to inherently short-term expenses. In this sense, the business pays and immediately receives the full value of what it is paying for. On the other hand, CapEx covers items like equipment and property, which require extended periods of time to reach their maximum utilization. To calculate using this method, first subtract the salvage value from the original purchase price.

Are there any drawbacks to Accelerated Depreciation?

When you go through the financial statements, quickly check what type of accounting method is used. Then compare it to a competitor and see whether it is inline with industry standards and suitable for the business model. At the beginning of the life, the accelerated method obviously costs more but towards the later stages of the useful life, the expenses become much less. If the straight line method was used, the depreciation would be constant and the maintenance cost would increase which would increase the total expenses. Accelerated depreciation will offset the increasing maintenance cost and essentially equalizes the combined charges of both maintenance and depreciation. The graph below is a simplified view of how the accelerated depreciation and maintenance cost works out to give a straight line total expense.

Other depreciation methods

- While the purchase price of an asset is known, one must make assumptions regarding the salvage value and useful life.

- Calculation of Accelerated Depreciation is more complex with while the straight-line depreciation is simple and easy to understand.

- Then compare it to a competitor and see whether it is inline with industry standards and suitable for the business model.

- Under the Declining Balance method of depreciation, benefits are higher at the beginning of an asset’s useful life and then decrease over time.

- Through depreciation, companies spread the cost of big purchases over the item’s life.

Depreciation means reducing the value of an asset for business and tax purposes. Most businesses have assets they need to depreciateStraight-line depreciation is a common method. The total dollar amount of the expense is the straight line depreciation vs accelerated same, regardless of the method you choose. An asset’s initial cost and useful life are also the same using any method. The total depreciation over the asset’s useful life is $40,000, and the machine produces 100,000 units.

In the short term, there can be income tax benefits to using this method. The expenses are then lowered as the asset is used less later in its lifespan. There are several calculations available for accelerated depreciation, such as the double declining balance method and the sum of the years’ digits method. If a company elects not to use accelerated depreciation, it can instead use the straight-line method, where it depreciates an asset at the same standard rate throughout its useful life.

In such cases, an accelerated depreciation method might provide a more realistic picture of an asset’s value and expense recognition. Depreciation is a fundamental concept in accounting and finance, representing the allocation of an asset’s cost over its useful life. Among the various methods available, straight line depreciation stands out for its simplicity and consistency. It is the most commonly used and straightforward method, where the asset’s cost is evenly spread over its expected life span. This approach assumes that the asset will provide equal value to the company each year, leading to a uniform expense charge in the income statement.

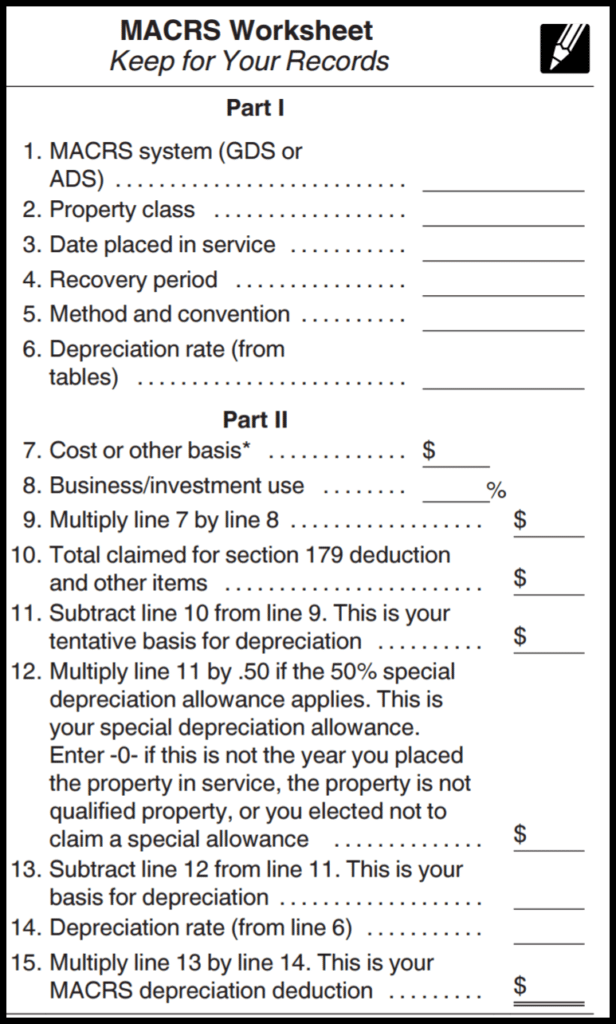

By using this formula, you can calculate when you will need to replace an asset and prepare for that expense. Accelerated depreciation, especially the Modified Accelerated Cost Recovery System (MACRS), is vital for managing assets. This helps companies delay tax payments and encourages investment in key areas like renewable energy, especially during tough economic times.

It’s a decision that should be made with careful consideration of all these factors, ideally in consultation with financial advisors. Remember, the method you choose will not only reflect on your balance sheet but also signal your company’s financial approach to stakeholders. Choose wisely, as it will shape your financial narrative for years to come. Depreciation is a critical concept in accounting and finance, representing the allocation of an asset’s cost over its useful life.

A company with a strong cash flow might prefer the straight-line method to smooth out expenses, while a startup looking to minimize taxes in its early years might opt for an accelerated method. Understanding accelerated depreciation versus straight-line method is vital. It’s important to choose the right method to improve a company’s financial health. The common method of accelerated depreciation is called the double declining balance (DDB) method.

While the purchase price of an asset is known, one must make assumptions regarding the salvage value and useful life. These numbers can be arrived at in several ways, but getting them wrong could be costly. Also, a straight-line basis assumes that an asset’s value declines at a steady and unchanging rate. This may not be true for all assets, in which case a different method should be used.

Business leaders must weigh the pros and cons of methods like the double declining balance and MACRS against simpler methods. Instead, the cost is placed as an asset onto the balance sheet and that value is steadily reduced over the useful life of the asset. This happens because of the matching principle from GAAP, which says expenses are recorded in the same accounting period as the revenue that is earned as a result of those expenses. Straight-line depreciation is a common method of depreciation where the value of a fixed asset is reduced evenly over its useful life. The method was developed to give a picture of the consumption pattern of the asset involved. It is generally used when there is no pattern on how you use an asset over time.